Recebido: 9-04-2022 | Aprovado: 24-06-2022

![]() Naoufel Belhaj, Cadi Ayyad University, Marrakech, Morocco (belhaj.naoufel@gmail.com)

Naoufel Belhaj, Cadi Ayyad University, Marrakech, Morocco (belhaj.naoufel@gmail.com)

How to cite this article:

Belhaj, N. (2023). Local taxation and sustainable urban development in Morocco.

RevistaMultidisciplinar, 5(1), 55-70.

https://doi.org/10.23882/rmd.23109

Abstract: Over the last few decades, the financing of cities has been at the heart of ongoing debates of change and deep reforms as well as major concerns in all countries where decentralization is giving an increasingly dynamic role to local governments. This article presents the role of local taxation in promoting sustainable urban development in Morocco through an empirical study of 163 actors and partners involved in cities in the regions of Casablanca-Settat and Rabat-Salé-Kénitra. The results show that to increase local taxation in Morocco, it is necessary to develop the capacity of city managers, encourage public-private partnerships, and improve the quality of spending.

Keywords: local taxation, sustainable urban development, cities, Morocco.

Introduction

Sustainable

urban development is an integration of the concept of sustainable development

with an operating mode of spatial planning: urban planning. These two concepts

have a common objective, that of a harmonious development of the citizens in a

well determined space: the city, answering their needs namely: housing,

employment, education and access to leisure, in an economically attractive,

politically stable and culturally rich universe (Camagni & Gibelli, 1997).

It is also a system that independently articulates elements of the three

pillars: the economic pillar, the social pillar and the environmental pillar

(Didier, 2007, p.11), « the sustainability

approach establishes […] public policies that make it possible to articulate the

socioeconomic development and spatial planning of urban areas with careful

management of the environment» (Bochet & Cunha, 2002, p. 3).

However, to promote

sustainable urban development, to support urban growth and socio-economic

development, as well as to improve the quality of life of city dwellers, it is

necessary to seek effective and innovative financing mechanisms, appropriate

financial governance mechanisms and adapted legislative and institutional

frameworks. The objective is to promote equitable and environmentally friendly

socio-economic development, by promoting the attractiveness of cities and

supporting the creation of businesses and jobs.

Sustainable

urban development can only be conceived in a context where the local economy is

consolidated. Therefore, it is essential to establish a good quality

infrastructure environment. The realization of infrastructure and public

investment is globally through three sources (Yatta, 2014):

1.

Financial transfers from

the state to cities, which can take several forms: general allocations to

finance certain investments or support certain policies, subsidies to balance

the budgets of local governments, etc…;

2.

External resources made

up of loans;

3.

Revenue from local

privatization and public-private partnerships, which also contribute to the

financing of local public investments.

The fact

remains that mobilizing local tax potential is the key to local socio-economic

development. The weakness of the city's financial resources is more often linked

to the low actual level of local taxation than to the economic poverty of local

authorities. Several sectors of the economy are taxed very little or not at all,

while land assets do not contribute enough to local economic activity. These

findings indicate that most cities in developing countries are actually poorer

than their inhabitants. A study about local finance in these countries concluded

that it is possible to strengthen local resources considerably while maintaining

the same level of local taxation (Bahl & Linn, 1992, p. 385-427).

They argued that the less cities collect and

spend, the poorer they become, and that «They

argued that the less cities levy and spend, the poorer they become, and that

"the inability of local governments to spend creates a vicious cycle in which a

poor living environment leads to stagnation and even relative regression in the

local economy: the more cities levy and spend, the better off the local economy

becomes» (FMDV, 2014, p.12).

We will

present a review of the literature and an overview of local taxation in Morocco.

We will then present the methodology adopted and conclude with an analysis and

discussion of the results on the causes of the weakness of local taxation in

Morocco and the tools to strengthen it in order to improve the financial

autonomy of cities and promote sustainable urban development.

1. Literature Review

The

development of cities' financial resources is a major concern of local

decision-makers in order to meet the increased needs of citizens and promote the

socio-economic development of urban centers. Generally, these financial

resources are made up of own or local resources; borrowing resources; financial

contributions from the State "Ministries and Public Companies"; local

privatization revenues (asset sales, public-private partnerships, public service

concessions) and donations and bequests (FONDAFIP, 2015).

In Morocco,

the 2015 reports on local taxation by the Regional Courts of Accounts indicate

that there is significant urban tax potential, but its exploitation is very

weak, both in terms of the tax base and collection. Indeed, economic development

and rapid urban growth are not reflected in local tax revenues (Cour des Comptes, 2015). According to the situation of

revenues and expenditures of local governments in 2022, the resources

transferred by the State to local governments, consisting mainly of their share

in the prοduct of VAT, represent (56,7 %) of all local

tax revenues, followed by resources managed directly by the municipalities (33,7

%), then by resources managed by state services for the benefit of local

governments (9,6 %) (TGR, 2022). This reveals that the cities depend heavily on

financial support from the state (FONDAFIP, 2015). As a result, local

governments must make more efforts to develop their own sources of revenue.

Table 1

Evolution of local government resources between 2021 and 2022 in millions of

dirhams and in %.

|

Local

government resources |

|||

|

|

2021 |

2022 |

Evol. |

|

Transferred

resources |

2 186 |

2 084 |

- 4,7 % |

|

Resources

managed by state services for the benefit of local governments |

515 |

354 |

- 31,3 % |

|

Resources

managed directly by the municipalities |

1 147 |

1 238 |

7,9 % |

|

Total |

3 848 |

3 676 |

- 4,5 % |

Source : TGR, 2022

This inadequacy of local finances in Morocco is

mainly due to a low level of local tax revenue, a higher level of operating

expenditure than investment expenditure and the inability to achieve the full

investment budget (FONDAFIP, 2015).

1.1.

Low yield from local taxation

According to a report by the Regional Courts of Accounts on the

evaluation of local taxation, the own tax resources of urban communes cover only

54% of operating expenses; the remainder is financed essentially by the VAT

transferred by the State (Cour

des Comptes, 2015). This low yield of local

taxation is mainly due to the absence of local tax application circulars (FMDV,

2014), the lack of collection of local debts, the weak use of information

technology and exploitation of databases (Safir, 2015), the lack of qualified

human resources capable of managing the local tax base and monitoring their

collection (FONDAFIP, 2015), the lack of accountability, responsibility, and

coordination between the different actors in the city, as well as the low

quality of public services (Dedehouanou,

2019).

1.2.

The superiority of operating expenditures over investment expenditures

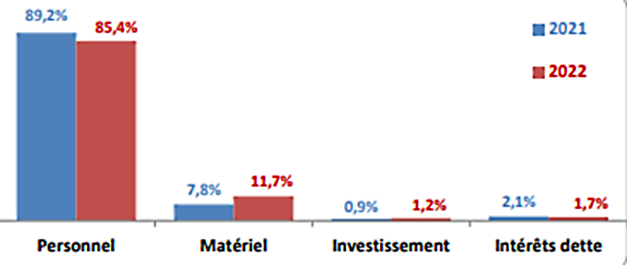

The

evolution of the structure of local government spending between 2021 and 2022

shows an increase in the share of equipment spending and investment spending,

combined with a decrease in the share of personnel spending and debt interest

charges, as shown in the following figure: (TGR, 2022).

Figure 1

Structure of overall expenditure of local authorities between 2021 and 2022 in %

Source : TGR, 2022

1.1.

The inability to achieve the full investment budget

In

Moroccan cities, investment needs are very high. Indeed, local managers do not

always realize the full amount of their investment budgets, which usually

results in surpluses that are carried over from year to year (FONDAFIP, 2015).

According to a report by the Consultative Commission on Regionalization,

surpluses from previous years (carryovers), in 2014, reached 23,4 billion

dirhams (CCR, 2014).

According to a report on the financing of African cities, Moroccan

municipalities are characterized by a very low absorption capacity and do not

carry out their entire investment budgets. In fact, they often have surpluses of

30 to 40 percent compared to the amount of investments made (Paulais, 2012).

1.2.

Significant budget transfers from the State to the cities

Moroccan cities regularly receive tax transfers from the State on the basis of

simple, transparent and objective criteria, aimed at encouraging them to develop

their own local resources, improve their propensity to invest, meet citizens'

needs in terms of infrastructure and public services and achieve socio-economic

promotion of urban centers.

The

state is the main provider of financial resources to cities through the

allocation of 30 percent of the proceeds of the VAT as well as through the

institution of new taxes and fees. Any increase in state revenue systematically

generates an increase in the resources transferred to cities, and any decrease

automatically results in a loss of value (FONDAFIP, 2015).

This

weakness in the yield of local taxation, obliges local governments to seek

innovative financing to improve the profitability of local finances. Local

assets can therefore be an alternative that can compensate for the weakness of

tax resources.

Along with these challenges, we can add:

·

The existence of spatial and socio-economic

inequalities between municipalities (Raiss, 1999);

·

Inequality in the distribution of resources between

the State and local authorities (Yatta, 2014);

·

The absence of information systems (FONDAFIP,

2015);

·

The presence of a very large informal economy (FMDV,

2014);

·

Weaknesses in accounting and budget management ;

·

Weak control of local finances and identification of

taxpayers;

·

A low level of income among the local population

(PFVT, 2017);

·

Weak capacity of local government;

·

Low exploitation of local taxes;

·

Low exploitation of some local taxes, such as

property tax (FONDAFIP, 2015);

·

A lack of autonomy in determining the tax base and

rates (Yatta, 2014);

·

Irrationality in the allocation of local expenditures

(Agoumy

& Refass, 2012);

·

The lack of rationality in the overall management of human resources

(Safir, 2015);

·

The absence of a consolidated vision of revenues and expenditures for city

management;

·

A less developed institutional framework in favor of cities (FMDV, 2014);

·

Political resistance to descentralization ;

·

Weak identification and mobilization of cities' fiscal potential (Cour des Comptes,

2015);

·

Low local debt collection;

·

Low participation of the private sector in the financing and production of

the city (FONDAFIP, 2015);

·

Weak coordination between the various city actors (Beaupuy, 2008);

·

The absence of tools for good governance of local resources (Habitat III,

2016).

2. Materials & Methodology

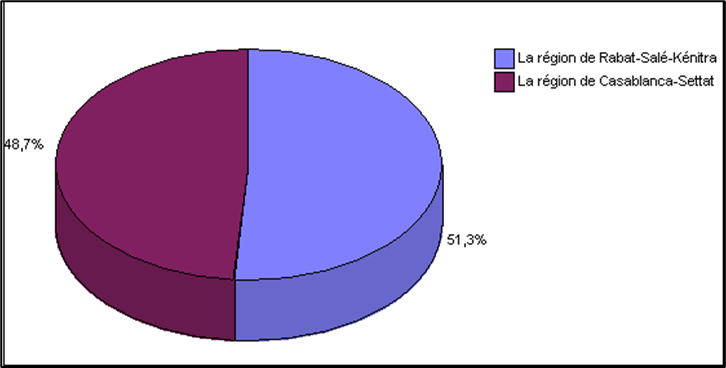

Our

sample is made up of 163 actors and partners involved in the cities in the

regions of Casablanca-Settat and Rabat-Sale-Kenitra. It is composed of 45 local

authorities, 6 national actors, 31 public institutions and companies, 18

regional and local actors, 7 international actors, 31 associations and 25

private companies. This sample is well distributed across the survey regions, as

shown in the table and graph below.

Table 2: Survey sample

|

who are

you? |

Number of observations |

Frequency |

|

Local authority |

45 |

27,6% |

|

National actor |

6 |

3,6% |

|

Regional and/or local actor |

18 |

11,4% |

|

Association |

31 |

19% |

|

Private company |

25 |

15,4% |

|

Public institution or company |

31 |

19% |

|

International actor |

7 |

4% |

|

Total |

163 |

100% |

Figure 2

Distribution of the sample between the regions of Casablanca-Settat

and Rabat-Sale-Kenitra

These data were processed using an exploratory data analysis method. We

used the stratified random sampling method, which gives the same chances to all

the units in the population and allows us to generalize the results obtained

from the sample.

In our case, the strata, which are heterogeneous groups, correspond to

the groups of actors: national actors, international actors, regional and local

actors, local authorities, civil society and private companies.

Among the 12 regions of the Kingdom, we chose the regions of

Rabat-Salé-Kénitra and Casablanca-Settat for several reasons, particularly their

demographic and economic weight compared to the other regions. Demographically,

the Rabat-Sale-Kenitra and Casablanca-Settat regions have 11,442,605

inhabitants, or 33.8 percent of the Moroccan population (HCP, 2014).

Economically, the regions of Casablanca-Settat and Rabat-Salé-Kénitra

create the most wealth and contributed the most to the national GDP in 2014,

These two regions alone contributed 48.3% of the national GDP (TGR, 2022).

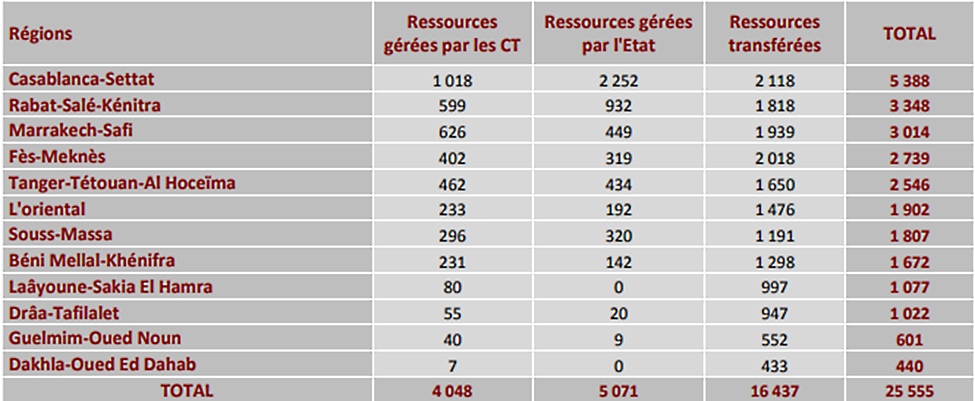

Table 3

Distribution of local government revenues by region

Despite their economic and demographic potential, these two regions depend heavily on financial support from the state and have a relatively low level of local taxation, hence the need for a profound review of the financial governance of the cities in these regions, in order to mobilize more resources and manage them better.

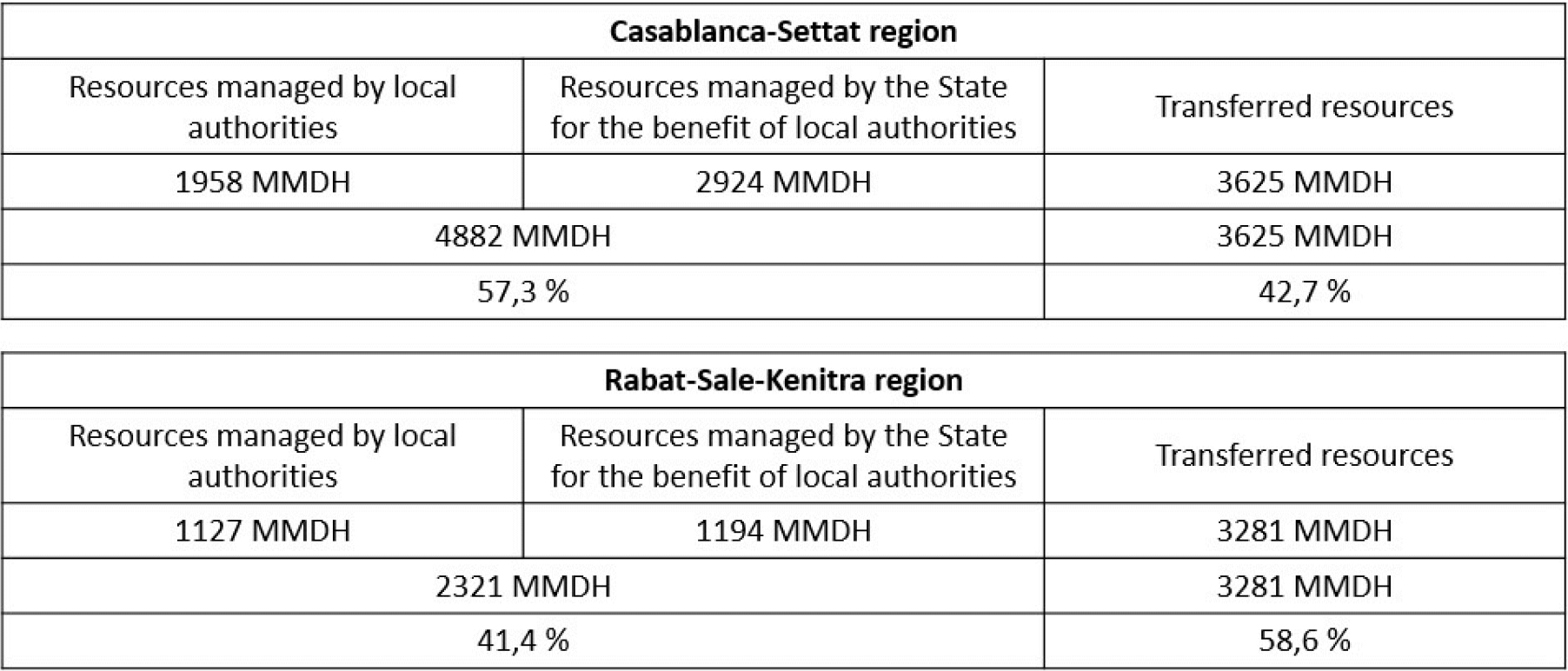

Table 4

Weight of local taxation in the budget of Casablanca-Settat and

Rabat-Sale-Kenitra regions in 2019, in millions of dirhams

Source: Author

3. Results, analysis and discussion

Local taxation represents an important part of the fiscal resources for local

governments, the other part being paid by the State within the framework of

decentralization laws. Local taxation concerns several urban sectors such as:

real estate, administrative, industrial, commercial, professional, transport,

tourism, etc.. (FMDV, 2014).

Cities in Morocco are highly dependent on financial support from the state and

are subject to the mutations and effects of globalization by transitivity. They

are influenced by the effects of the mobility of tax bases, due to the erosion

of the tax base and the transfer of profits. Almost 86% of the financial

resources of local authorities come essentially from revenues transferred or

managed by the State. This heavy dependence on state allocations puts local

governments at risk if the state's public finances do not generate sufficient

resources (FONDAFIP, 2019).

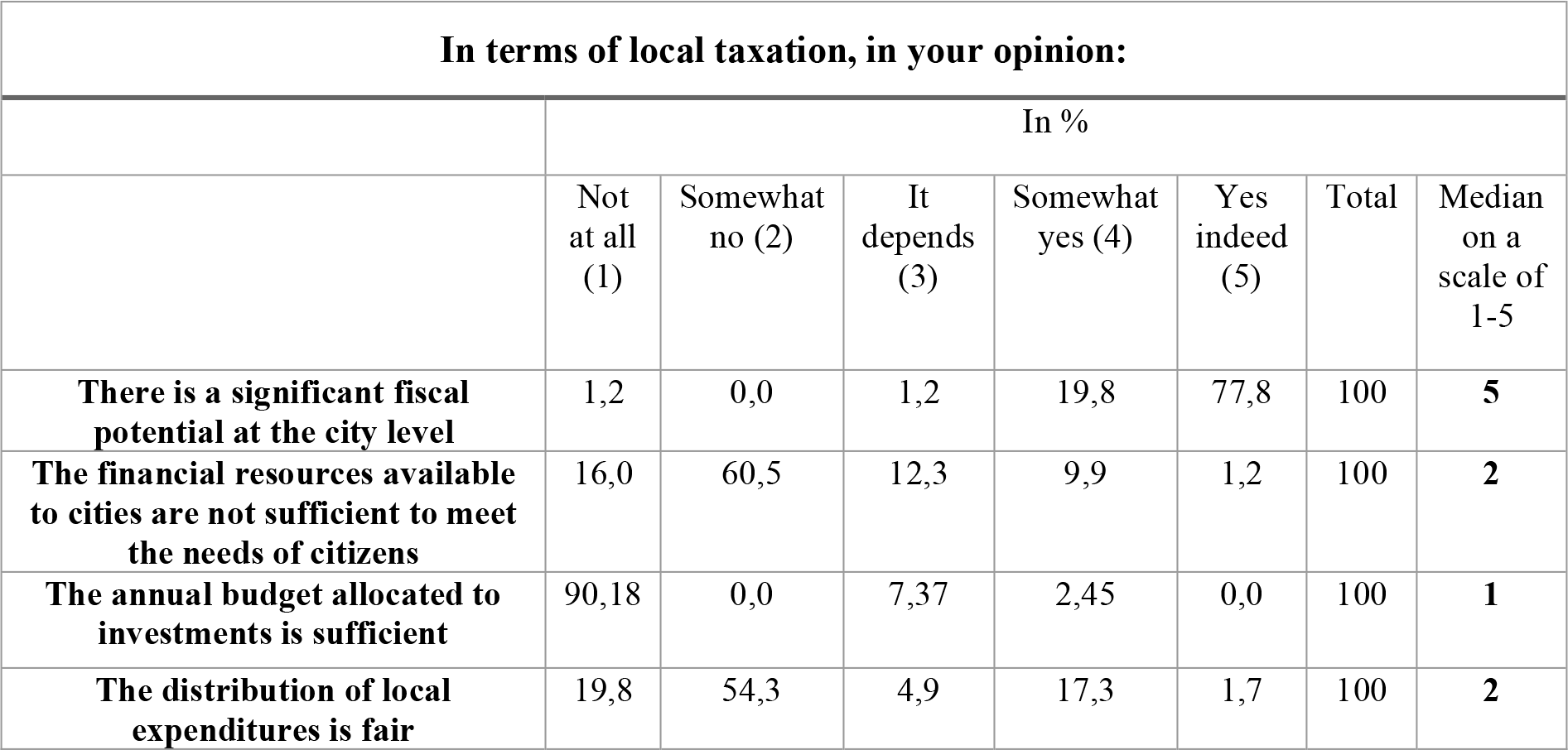

Among the shortcomings detected, almost all of the actors interviewed affirm

that there is significant fiscal potential in cities, but that it is poorly

exploited. The development generated by rapid urbanization and economic growth

is not reflected in local tax revenues. They also claim that the financial

resources available to cities are not sufficient to meet the needs of citizens,

that the annual investment budget is not sufficient, and that the distribution

of local expenditures is not equitable.

Table 5

City actors' perception of local taxation

The actors interviewed said that in order to

develop the financial resources of cities, it is necessary to improve the base

and/or rates of local taxes, increase local fees, improve the collection of

local taxes, encourage borrowing and strengthen public-private partnerships.

They also affirmed that it is the real estate sector that brings in the most

revenue from local taxation (taxes on edifices, constructions, subdivisions,

subdivision operations and undeveloped land), followed by the industrial sector

and finally the commercial sector.

Other questions were asked only to the local

authorities in order to find out what tools they use to make taxpayers aware of

the payment of local taxes, among the tools mentioned we can mention

communication around projects and sources of financing, dialogue with

representatives of the different professions, the intervention of the tax

department and legal tools, etc...

The local authorities also mention that they

have difficulties in identifying taxpayers, this is mainly due to the lack of an

updated database, the low tax civic-mindedness of citizens, internal fraud and

the low collaboration of taxpayers.

Also, local authorities say that they do not

have sufficiently qualified human resources to manage the local tax base and

monitor their collection, and that they do not make sufficient use of

information, communication and database technologies.

In order to increase a city's financial

autonomy, it is necessary to guarantee sufficient financial resources to local

managers to enable them to carry out their missions, and among them, local

taxation. The financing of investments, goods and public facilities is ensured

by local authorities through the collection of local taxes. A positive dynamism

of tax revenues makes it possible to constitute the guarantees necessary to

mobilize additional funds. In addition, local taxation aims to reduce

inequalities through the redistribution of income from assets and economic

activity within the city. It plays a central role in strengthening the city's

financial autonomy, in the structure of local budgets and in the construction of

local democratic life (AREA, 2003).

Therefore, in order to obtain additional

financing, local and regional governments must be made more attractive to

investors (a solid fiscal base and good local financial governance). In addition

to private operators, cities need to diversify their sources of funding,

especially from international donors (international markets, finance companies

and commercial banks). This allows them to mobilize significant funds to finance

large-scale projects.

Improving the quality of spending contributes to citizens' acceptance of

taxes. "The inability of local governments to spend creates a vicious cycle

in which a poor living environment leads to stagnation or even relative

regression in the local economy: the less a city levies and spends, the poorer

everyone ends up being" (FMDV, 2014, p.12). Cities can double or even triple

the level of levies and spending to make the local economy better off. But such

an ambition requires dialogue between local managers and local

socio-professional groups, as well as efficient and transparent management of

the resources collected. Managers need to balance elective and participatory

democracy to increase fiscal efficiency: citizens have more incentive to pay for

services that meet their priorities, especially if they have been involved in

the decision-making process regarding the provision of these services.

Improving the quality of spending is closely linked to the establishment

of effective systems of local financial control to ensure good local management.

The local tax system applied to land, buildings, subdivisions and

undeveloped land makes it possible to mobilize significant resources and to

finance public urban development facilities, such as roads, networks and

infrastructure. These expenses are so important that they cannot be covered

solely by local taxation, nor by the local authority budget. It is therefore

necessary to think about new and innovative financing mechanisms to involve

private operators in the financing of public facilities. These mechanisms would

make it possible to mobilize additional resources within contractually

negotiated frameworks and to improve the effectiveness and efficiency of the

construction of these facilities.

Improving local taxation also requires developing the capacities of city

managers and the skills of local authorities in defining the tax base and tax

rates. The city must therefore support and develop the capacities of local

managers (elected officials, executives, financial managers) through training

and the use of intermediaries and experts, "Our cities today have a greater

need for competent and qualified manager-strategists, capable of transforming

our cities into islands of prosperity, expertise, competitiveness and innovation"

(FONDAFIP, 2015). This will allow the city to improve the effectiveness of

the consultation of these local actors, and thus improve the mobilization and

management of local assets.

The main contribution of this publication is to confirm the positive

impact of improving local taxation on city financing and thus on sustainable

urban development. It is therefore essential to develop the capacities of city

managers, encourage public-private partnerships and improve the quality of

expenditure.

Conclusion

Local taxation in cities in developing countries has many shortcomings, and its

revenue does not sufficiently feed the local budget. This is due to a number of

factors, including the existence of a less developed institutional framework for

cities, a low level of income among citizens, poor use of some local taxes,

inequality in the distribution of resources between the central government and

local authorities, political opposition to decentralization, erosion of the tax

base due to certain national policies, weak autonomy of local authorities, weak

local government capacity, and lack of confidence in local authorities on the

part of citizens and investors (AREA, 2003). In these countries, the collection

of local taxes is often poor, mainly due to the lack of suitable instruments for

determining tax potential, the complexity of tax assessment methods and the

definition of the tax base, and the difficulties of issuing tax rolls and

collecting them.

In

most developing countries, it is the state that determines the base, rate and

basis of local taxes. Thus, cities are entirely passive in determining what

constitutes the basis of their financial autonomy. Generally, there is no

contractual relationship between the state departments and the local governments

for which they are supposed to work. The latter have no possibility of reacting

to underperformance on the part of the state departments (Jnah, 2018).

Nowadays, financing has become a fundamental element in the problem of urban

governance. Indeed, urban sprawl, spatial dispersion, concentration of

employment locations, and movement of inhabitants often pose a problem of

financing public services and infrastructure (OCDE, 2019). There is a need to

provide cities with the necessary and sufficient funds to meet the increased

expectations and needs of citizens and businesses. Cities must therefore

consider, in coordination with relevant stakeholders and the local population,

operational taxation strategies to mobilize financial resources that will allow

them to meet the expectations and needs of their residents and properly carry

out their missions (FONDAFIP, 2015).

The

problem of financing cities is not only about the availability of financial

resources, but also about their mobilization, management and direction (FMDV,

2014). Therefore, cities must effectively manage local financial resources while

adhering to the principles of integrity, transparency, participation, democracy,

accountability and equity (Moindze, 2010). Furthermore, the implementation of

sustainable urban development must be accompanied by sufficient financial

resources and appropriate governance of these resources. The objective is to

promote the socio-economic development of cities, fostering their attractiveness

and competitiveness and supporting the creation of businesses and jobs.

Strengthening the financial system of Moroccan cities and regions requires a

more balanced sharing of powers and financial resources between the State and

local authorities. It is necessary to encourage local authorities to broaden the

tax base and develop their local taxation, to increase borrowing and to seek

effective and innovative financing mechanisms, appropriate financial governance

mechanisms and suitable legislative and institutional frameworks. These

principles are all assets that confront the budgets of cities and regions and

that will make it possible to improve regional finances without increasing the

financial burden on the State. In this perspective, the encouragement of

investment and the creation of wealth are closely linked to national, regional

and local economic development.

References

Agoumy, T., & Refass, M. (2012). Ville et environnement durable en Afrique et

au Moyen-Orient. Publications de la Faculté des Lettres et des Sciences

Humaines, Rabat.

AREA, Atelier de Recherches, d’Etudes et d’Architecture (2003). Etude

relative au financement et à la maîtrise du coût de l’urbanisation.

Commanditaire : Ministère chargé de l’Habitat et de l’Urbanisme, Direction de

l’Urbanisme, Maroc.

Bahl, R. W., & Linn, J. F. (1992). Urban public finance in developing

countries. The World Bank.

Beaupuy, J-M. (2008). Bâtir des villes durables. Yves Michel, Paris.

Bochet B., & Cunha A. (2002). Développement urbain durable. Vues sur la ville,

(1), 3-5.

Commission Consultative de la

Régionalisation (CCR), Rapport sur la régionalisation avancée, 2014, [en ligne],

https://bit.ly/3A4URPV

Cour des Comptes (Ed.) (2015). La fiscalité locale : synthèse. Royaume du

Maroc. https://bit.ly/3QO6MHJ

Didier C. (2007). Le développement urbain durable : pour une approche

différente de la vie urbaine. Thèse de doctorat sous la direction du

Professeur Bernard LAMIZET, Soutenue le 30 août 2007, Université Lyon 2,

Institut d'Etudes Politiques de Lyon.

FMDV (2014). Renforcer les recettes fiscales locales pour financer le

développement urbain en Afrique, Paroles d’acteurs locaux - Etude de cas des

stratégies de 8 villes africaines. Fonds Mondial pour le Développement des

Villes & Ministère des Affaires Etrangères Français. https://bit.ly/3OFuILt

FONDAFIP (2015). La gouvernance financière au Maroc et en France. 9éme

édition du Colloque International des Finances publiques, Rabat.

Habitat III (2016, Mars 9-11). Financement du Développement Urbain : Le Défi

du Millénaires. Réunion Thématique d’Habitat III, Note de synthèse, México

City.

HCP (2014). Recensement Général de la Population et de l'Habitat de 2014.

Haut-Commissariat au Plan

HCP (2018). Le Maroc en Chiffres. Haut-Commissariat au Plan

Moindze, M. (2010). Les standards internationaux de la bonne gouvernance des

finances publiques. https://bit.ly/3y0HWMq

OCDE (2010). Conduire les politiques de développement régional ; Les

indicateurs de performance. OCDE.

PFVT, Partenariat Français pour

les Villes et les Territoires (2017). Le financement local, condition du

développement territorial durable et inclusif. conférence Habitat III vers

la définition d’un nouvel agenda urbain.

Safir, K. (2015). Casablanca, Hub Financier International Connecté et Inclusif.

9ème édition du Colloque International des Finances publiques, Rabat.

Trésorerie Générale du Royaume (TGR) (2022). Bulletin mensuel des

statistiques des finances locales. TRG.

Yatta,

F. P. (2014). La gouvernance financière locale. Partenariat pour le

développement Municipal (PDM). https://bit.ly/3neSIth